I would like to share with you my experience in sueing Lloydstsb over my overdraft

charges.

My name is Barry Wood and if you want to email me email alphablending2001uk@yahoo.co.uk

Making a request under the Data Protection Act

Currently Lloydstsb are asking people to pay Ł5 for each replacement paper statement that they print out. This can

very costly as most people don't keep statements from 6 years ago. So for myself I decided to request a list of all my

charges under the data protection act (they are legally allowed to take up to 40 days). You can asked them for a list of

charges but not the statements themselves. I put in a request at Lloydstsb's branch in King's Lynn, Norfolk and had no

communication with them until my father receieved a phone call about 38 days later say that my information was ready to

be picked up. As I rust to the bank to collect up my info I wondered to myself how much they had charged me. I thought it

might be something around Ł1000 maybe Ł1500. As I sat down in Macdonlds sipping my coffee; I opened the packed and started

adding it up in my head I couldn't beleve the amounts that were taken on each date the list justed seemed to go on. I went

home and added it up on my computer. For a Ł1500 overdraft they had charged me Ł2790.

Summary

You can only ask for a list of charges under the Data Protection Act

You will possible be charged Ł10 for the list of charges

They legaly have 40 days to comply and expect to wait that long! (if it goes over 40 days kick up a fuss

Put your request in at a Bank and don't accept it if they say it's going to cost Ł5 per statement

First Letter and Response

After I added up all of my bank charges it was time to right a letter to Lloydstsb asking for my bank charges back.

I got a template of www.fool.co.uk. It was written as follows:

Dear Sir/Madam

Account no: 00000000, Sort Code: 000000

Over the past six years, you have charged me for exceeding my credit limit. It has come to my attention that this is unlawful at common law, and under statute and recent consumer regulations.

In the terms of the contract which you agreed to at the time that I opened my account, it is implied that you will conduct yourselves in a manner which complies with UK law.

Unless you can prove that they merely cover your administrative costs, I require full repayment of these charges, which I calculate at Łxxxx plus interest of Łxxxx. The total is xxxx. I also ask you to remove any default notices on my credit record that are related to these charges. A correction or amendment to the entries is not acceptable.

If you do not comply fully within 14 days, I shall begin a claim against you for the full amount, plus interest and costs, plus I shall submit a complaint to the Information Commissioner.

Yours faithfully

Xxxx

I would suggest if you want to send this of send it by recorded signed for as you can track it and the day of delivery on

the Royal Mail's websites. I sent a copy off to Lloydstsb main address on their website but it never arrived so I rang them

up and asked them were to send the request they gave me this address:

Customer Service Recovery Centre,

Charlton Place,

Andover

Hampshire

Hampsire

SP10 1RE

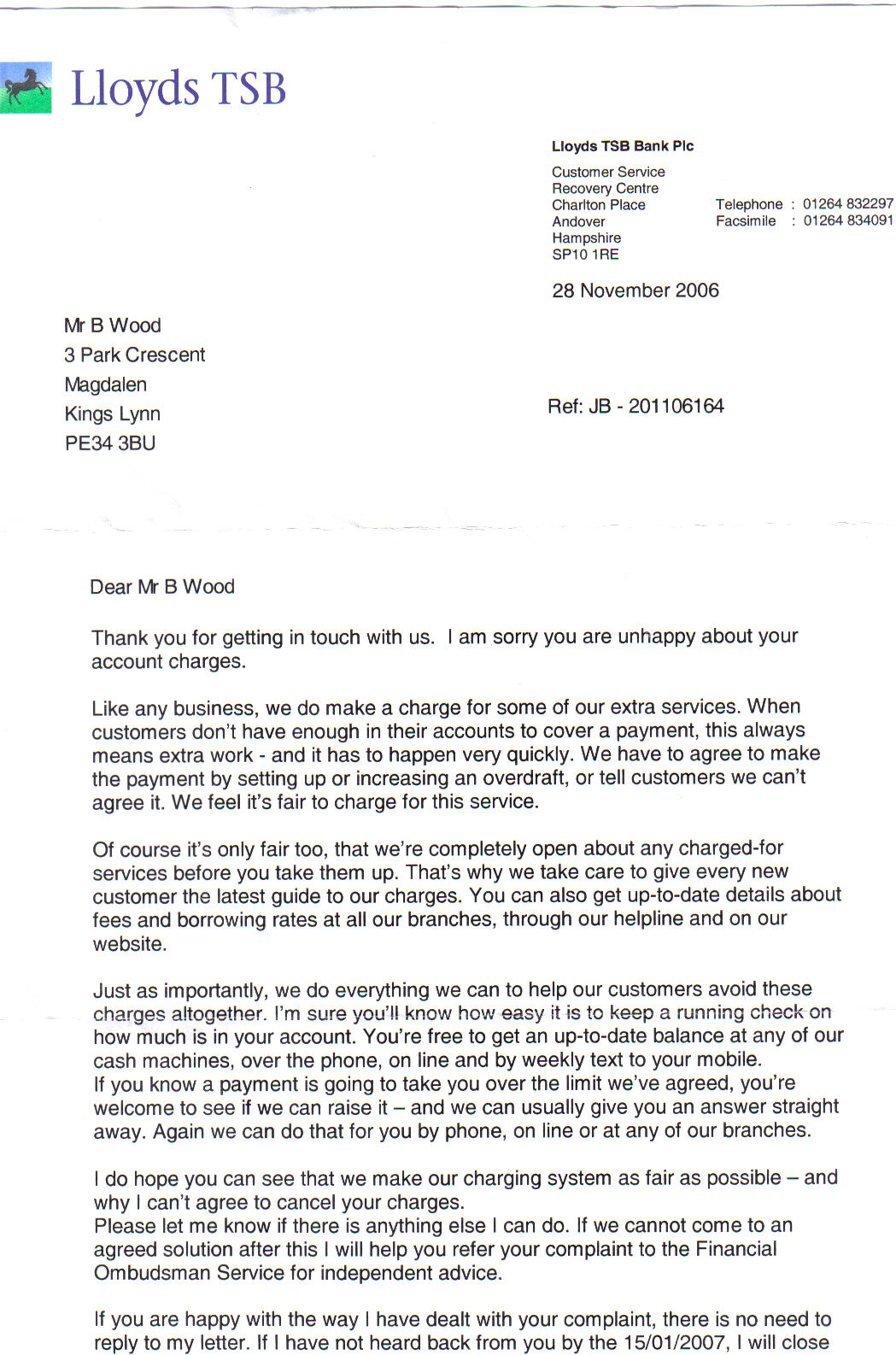

The first letter back

About 15 days later I received a letter back saying the standard stuff like these charges are fair (NOT!) and that it is

easy for you to check to see if you are going over. The following is the letter I was sent back:

This letter is template that the Lloydstsb sends out automatically. I know this because it reads as if I have an account

and I actually closed it about 4 months before doing this and the signiture is a photocopy. I totally iginored this letter

and began to wright another.

Second Letter and Response

The second letter is called the letter before action. It tells the bank basically give me back my money or get sued I sent

it in the same way and to the same address as before:

Dear Sir/Madam

Account no: xxxxxxxx

I am disappointed that you have not agreed to refund the charges on my account in relation to direct debit refusals, exceeding overdraft limits and so forth, despite the fact that they are unlawful at common law, under statute and under recent consumer regulations.

I would draw your attention to the terms of the contract which you agreed to at the time that I opened my account. It is an implied term of that contract that you would conduct yourselves lawfully and in a manner which complies with UK law. I am frankly shocked that you have operated my account in this way.

I calculate that you have taken Łxxxx plus Łxxxx which you have charged me in overdraft interest for the sum which you have taken. Total Łxxxx.

I am enclosing a copy of the schedule of the charges which I am claiming.

I require repayment in full of this money and removal of the default notice. If you do not comply fully within 14 days then I shall begin a claim against you for the full amount plus interest plus a claim under ss.7 and 13 of the Data Protection Act 1998 plus my costs and without further notice.<\A>

Yours faithfully

xxxx

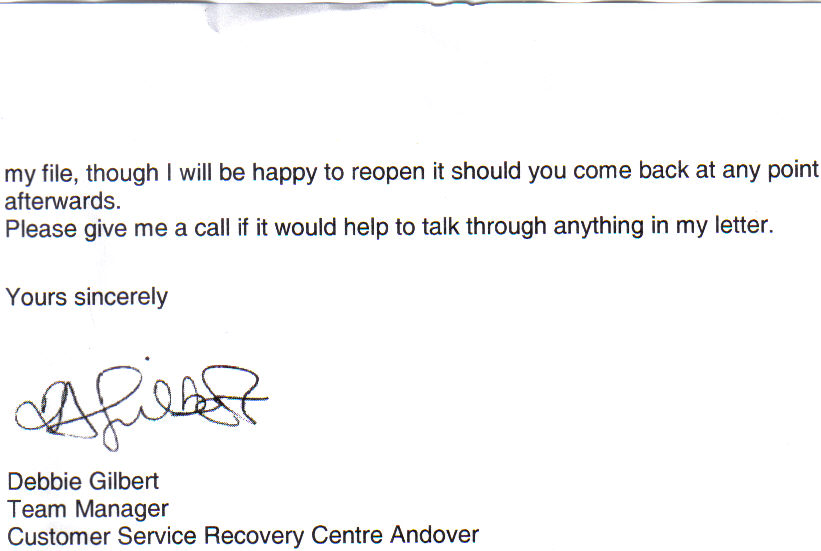

The second letter back

The letter I send was a letter before action Lloydstsb's letter was there last one it went as follows:

As you can see they are trying to negotiate with me (this is a bullying tacktick). I have read on so many websites that

banks will try and settle for less than the amount as this look as if this is the banks final offer. Its not. They owe me

this money because they have taken it illegally and to anyone else there that feels unsure about settling don't!!!!. It's

you money and settling is just like saying to the banks have my money its yours and that just isint the case.

Court Poccedings & moneyclaimonline.com

As Lloydstsb will not give me my money back and the 14 days have expireed it is now time for me to take it to court. DON'T

WORRY if you are at this stage as it is easy!. I used www.moneyclaim.gov.uk to issue court poccedings. I started an

account with them as a claimant and started entering the information as requested. Most of it's straight forward so I don't

really need to get into it but there are two parts that are a little bit confusing the claim part and the judgment.

Claim

The claim part is where you actually enter what is owed and the reason why. I again modified a templete of

www.fool.co.uk.

for this and changed it accordingly. It follows as:

The Defendant has imposed charges of around

Ł30 each time the Claimant has exceeded his

overdraft limit, had a cheque return or

direct debt refused.

These charges represent a penalty and do

not accurately reflect the Defendant's

administration costs. Further,

they are contrary to the Unfair (Contract)

Terms Act 1977 s.4 and the Unfair Terms in

Consumer Contracts Regulations 1999. para.

8 and sch. 2(1)(e). Further or

alternatively, they are unreasonable within

the meaning of the Supply of Goods and

Services Act 1982 s.15.

The total charges he is claiming are

Ł3000.00. The

claimant claims interest under section 69

of the County Courts Act 1984 at the rate

of 8% a year from the dates that each of

the charges were made, AND THE CLAIMANT

As you can see there is a lot of legal gargon and to be honest I don't under stand it all bur the guy that wrote

www.fool.co.uk.

used a simuler template and got all his money back. In the statment you can see that I have asked not only

for my money back but also my court fees and also for 8% of my charges back as well. I might be strange but under law you

can do this as this is interest on the amount they owed you. To be honest again I haven't got a clue how to work it out

but I was told that if I over estimated and I went to court (which would'nt happen) the judge would change the amount

change it if it was incorrect. I would recommend overestimating it as the judge will only bring it down but change it up.

Judgement

This section is completed by the claimant (me or you) and is only completed if the bank does not send a response within

the 14 days required or it is completed by the claiment if the bank says that they owe the claiment the money

(I don't think this will happen). I also found out that is when the claim form gets to the bank and not when you active

and pay for the claim.

UNDER CONSTRUCTION!

Free Counter