MONEY: A financial asset that makes the economy

function

smoothly by

serving as:

1. A medium of exchange

2. A unit of account

3. A store of wealth

FUNCTIONS OF MONEY EXPANDED:

Medium

of

Exchange

Lubricates exchange (vs. barter)

Accepted as payment for debt

Faith => fiat money, by decree -- not backed by gold

Optimum Scarcity

too much -- goods sell fast => prices rise

too little -- barter, goods sell slow => prices fall

limited supply

hard to counterfeit

Unit

of

Account

If money is stable it is accepted as deferred payment

problematic w/ hyperinflation => if pay back is in cheap

money (reference lost)

Provides relative price information

cigarettes during WWII & jail

Store

of

Wealth

A bond that pays no interest

Coffee cans & mattresses

Liquid debt

w/ gp people spend $ quickly

w/out gp people spend $ slower

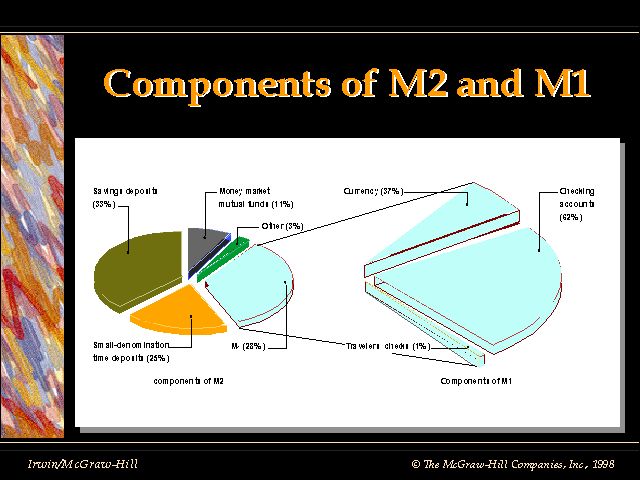

DEFINITIONS OF MONEY: based on liquidity

Liquidity: the ability to turn an asset into cash quickly w/out losing

value. Cash is the ultimate liquid asset.

M1 = currency (nonbank), demand deposits

(checking

accounts) &

travelers' checks

M2 = M1 + savings deposits, small time deposits,

money

market mutual

fund shares, money market deposit accounts, overnight repurchase

agreements, overnight eurodollars

M3 = M2 + large time deposits (negotiable, Jumbo

CDs),

money market

mutual fund shares (institutions only) & term repurchase

agreements

L = M3 + short-term Treasury securities,

commercial

paper, term

eurodollars, savings bonds & bankers acceptances (buyer's IOU

may not be accepted by seller, but the buyer's bank gives its IOU)

****************************************************************

Credit Cards -- why aren't they counted?

Credit

is savings

made available to be borrowed => already counted

Asset Management -- banks handling of loans & other assets

Liability management -- how a bank attracts

deposits

& what it

pays for them

HISTORY OF BANKING => short course

Marco

Polo

- Kubla Khan

Goldsmiths

- Modern Banking (fractional reserve baanking)

HOW BANKS CREATE MONEY:

Remember: Financial assets can be created as long as an offsetting financial liability is simultaneously created.

Reserve

Requirement = r (or rr, this is set

by the Fed)

(required

reserves)

r not counted as money

England has no r

Legal Reserves = Required Reserves + Excess

Reserves

*Out of legal reserves banks

can lend out excess reserves

****************************************************************

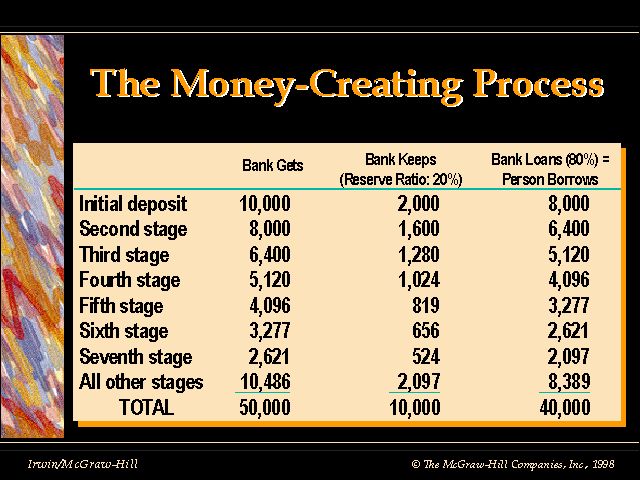

Example: T-Account w/ a deposit of $1,000 & r=.2

Assumptions: banks are profit seekers & are

fully

loaned out

there are no excess reserves

bank requires borrowers to open dd by the amount of loan

the intial deposit is new money into the system

ASSETS

LIABILITIES

$1,000 demand deposit/Bill

r=$200

$800 loan/Mary

$800 demand deposit/Mary

r=$160

$640 loan/Kim

$640 demand deposit/Kim

r=$128

$512 loan/Herb

*This process continues until the total reserve requirement (r) equals the initial injection of $1,000. Notice that including the original deposit a total of $2,440 in demand deposits has been created after just a few steps.

A simpler way of finding how much money will be created by this process is to multiply the simple money multiplier (m) times the initial injection.

m = 1/r => (m) x

(initial

injection) = money created

(5) x ($1,000) = $5,000

m = 1/r = 1/.2 = 5

initial injection = $1,000

WHAT ABOUT A WITHDRAWAL OF $1,000 OUT OF THE SYSTEM?

Let's say Bill withdraws the original $1,000 & takes it completely out of the system:

The only thing left to cover

the

withdrawal is r = $1,000, therefore there

is no r to cover the other demand

deposits of $4,000 and the bank must

call in its loans. The

demand

deposits go to zero. $5,000 in money has

been destroyed.

(m) x (withdrawal) = money destroyed

(5) x (-$1,000) = -$5,000

m = 1/r => what happens when r changes?

when r

falls m increases & when r increases m falls

****************************************************************

Complex m = 1/r+c, where c = ratio of cash to

deposits

Example:

$100 => $20 cash/$80 deposits = .25

r = .20

complex

m = 1/r+c = 1/(.20+.25) = 1/.45 = 2.1

*in reality complex m is much smaller

Your checking account is the liability of the

bank

secured by their assets

(loans). These loans are the financial

liability

of the borrower -- promises

to pay. Banks borrow short & lend long.

Runs on the bank -- FEAR -- FDIC & FSLIC

Failed S&Ls in the late 80s.

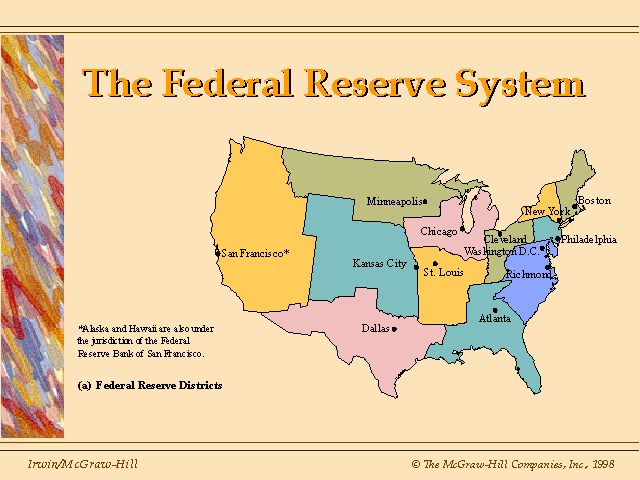

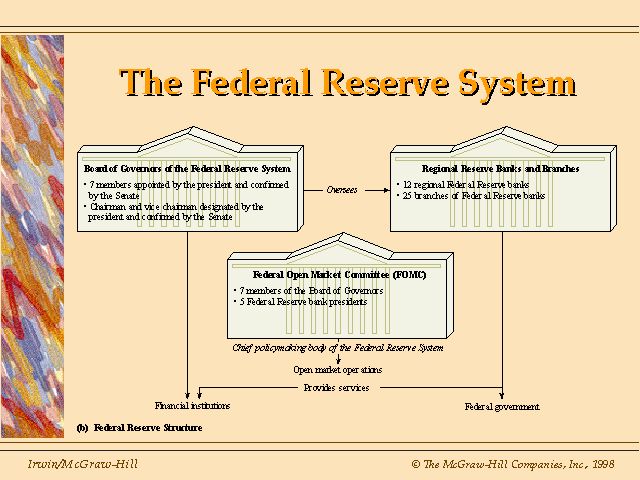

THE FEDERAL RESERVE SYSTEM

Central Bank

=>

The Bankers' Bank

*Conducts

monetary policy & supervises the financial system

European Central Bank

=>

Bundesbank

The Bank of Japan

Bank of England

Monetary

Policy:

Fed policy that influences the economy through

changes in the $ supply & available credit

THE FED

Quasi

government

organization: the government makes the major

personnel

appointments, but the Fed is privately owned by its

member banks

12 Regional Banks of the Fed

Board of Governors

=>

7 members

Appointed by the President

Approved by the Senate

Headed by

the Chairman (Alan Greenspan)

*all governors have 14 year

terms, except for the chairman who has a

4 year term

Policy

Making Body of the Fed

Federal Open Market Committee (FOMC)

Members of the FOMC:

Board of Governors (including the chair)

The President of the NY Fed

Four other Regional Bank Presidents (on a rotating basis)

FUNCTIONS OF THE FED:

1. Monetary Policy

(expansionary/contractionary)

2. Supervision &

Regulation

of Financial Institutions

3. Lender of Last Resort

4. Provides Banking

Services

to the Government

5. Issues Coin &

Currency

6. Financial Services

to Commercial Banks

TOOLS OF MONETARY POLICY:

1. Sets Reserve Requirement

2. Sets Discount Rate

3. Open Market Operations

*fighting recessions &

gp

M up

=> i

down => I up => Y up

M down

=>

i

up => I down => Y down

Keynesians target i

Classicals MV=PQ

(Rules)

SR effects on real output

LR => increasing M causes gp (affects only the price level)

Nominal vs. Real Interest Rates

Five Problems of

Monetary

Policy

1. Knowing what policy to use (correct Yp)

2. Understanding the policy you're using

the fed only controls vault cash & reserves @ the fed

called the monetary base

m influenced by cash people hold (moving target)

3. Lags in monetary policy

4. Political pressure

5. Conflicting international goals

Central Bank

=>

The Bankers' Bank

*Conducts

monetary policy & supervises the financial system

European Central Bank

=>

Bundesbank

The Bank of Japan

Bank of England

Monetary

Policy:

Fed policy that influences the economy through

changes in the $ supply & available credit

THE FED

Quasi

government

organization: the government makes the major

personnel

appointments, but the Fed is privately owned by its

member banks

12 Regional Banks of the Fed

Board of Governors

=>

7 members

Appointed by the President

Approved by the Senate

Headed by

the Chairman (Alan Greenspan)

*all governors have 14 year

terms, except for the chairman who has a

4 year term

Policy Making Body of the Fed

Federal Open Market Committee (FOMC)

Members of the FOMC:

Board of Governors (including the chair)

The President of the NY Fed

Four other Regional Bank Presidents (on a rotating basis)

FUNCTIONS OF THE FED:

1. Monetary Policy

(expansionary/contractionary)

2. Supervision &

Regulation

of Financial Institutions

3. Lender of Last Resort

4. Provides Banking

Services

to the Government

5. Issues Coin &

Currency

6. Financial Services

to Commercial Banks

TOOLS OF MONETARY POLICY:

1. Sets Reserve Requirement

2. Sets Discount Rate

3. Open Market Operations

*fighting recessions &

gp

M up

=> i

down => I up => Y up

M down

=>

i

up => I down => Y down

Keynesians target i

Classicals MV=PQ

(Rules)

SR effects on real output

LR => increasing M causes gp (affects only the price level)

Nominal vs. Real Interest Rates

Five Problems of

Monetary

Policy

1. Knowing what policy to use (correct Yp)

2. Understanding the policy you're using

the fed only controls vault cash & reserves @ the fed

called the monetary base

m influenced by cash people hold (moving target)

3. Lags in monetary policy

4. Political pressure

5. Conflicting international goals