INTRODUCTION

The Economy: is the institutional structure whereby individuals in society coordinate their wants & desires

Economics: is the study of the economy

1. How people go about making a living

2. How scarce resources are allocated

Every Society faces THREE

central coordination problems:

1. What

to

produce & how much

2. How

to produce it

3. For

whom to produce it

**********************************************

The Basic Economic Problem=> Scarcity

Scarce

resources & unlimited wants/desires

Capitalism allocates resources by a

pricing

mechanism

SCARCITY FORCES US TO MAKE CHOICES

SOCIETY GENERALLY PREFERS MORE TO LESS

The Amish at Nordstrom’s?

Who has done more for society – Mother Teresa or

Bill Gates? It depends on what "more"

means?

If it

means spiritual, then Mother Teresa has done more.

If it refers to material well being then Mr. Gates has

more.

Ä

the amount of resources depends on human ingenuity — technological innovation

Four Main Resources (inputs): Factors

of

Production

1. Land

2. Labor

3. Kapital

4. Entreprenuership

**********************************************

Adam Smith’s Invisible Hand

works when there is prices that send signals

referred to as the pricing mechanism

according to Smith the exercise of individual self- interest benefits society

CONSUMER SOVEREIGNTY: power to decide what is/is not produced

Theories -- Models – over simplifications /abstractions => putting theory in a contextual setting

CETERIS PARIBUS: everything else being equal

The Circular Flow Model of Goods & Services

Micro vs. Macro

ECONOMIC

ANALYSIS

Positive

vs.

Normative

objective

vs.

subjective

empirical

vs.

value judgement

The Art of Economics=> Integrating positive & normative

What do economists know? UNCERTAINTY -- things change!

***********************************************************************************************

PRODUCTION

POSSIBILIES

& OPPORTUNTIY COSTS

OPPORTUNITY COST:

The

quantity of a good that must be given up in

order to obtain a good

The foregone value of the nest best alternative

Opportunity Costs can be seen numerically by way of a:

PRODUCTION POSSIBILITY TABLE

like an input/output table

Opportunity Costs can be seen graphically by way of a:

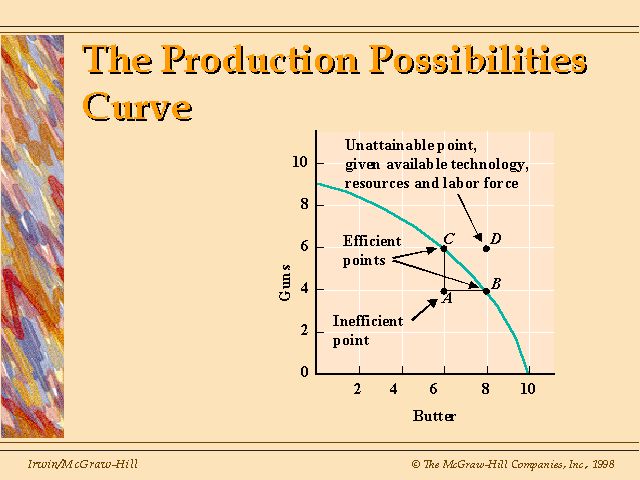

PRODUCTION POSSIBILITY CURVE

The table & the curve will show

different

combinations of output society can choose from. When society wants more

of one item then it must give up some of another item.

ASSUMPTIONS:

1. Full employment of all resources (in this case labor)

2. The level of technology is constant

3. Resources are interchangeable w/out inefficiency

4. Society prefers more to less

5. Society produces only tacos & tequila/no

trade

hrs. Labor Tacos hrs. Labor Tequila

20 200 0 0

15 150 5 15

10 100 10 30

5 50 15 45

0 0 20 60

Opportunity Cost of tacos for tequila

50 tacos/15 tequila (3.33 tacos for 1 tequila)

* if society wants tacos it must give up tequila -- just reverse the numbers

NEGATIVE SLOPE

* There is an inverse relation: to get more of one thing

you must give up something else

CONSTANT COSTS: all along the graph the opportunity cost is the same 50/15. This is represented graphically by a straight line PPC

Now, we will drop the assumption that resources are interchangeable, because some resources are better suited for the production of one good than another

COMPARATIVE ADVANTAGE (narrowly defined): To be better suited for the production one good than the production of another

Basketball Players & Jockeys

&

World’s fastest typist

Production Possibilities Table

Point

Missiles

Big Macs

A

3

0

B 2 10 billion

C 1 14 billion

D 0 15 billion

This implies... The Law of Increasing Costs, or,

The Law of Increasing Marginal Opportunity Cost:

to get more of something you have to give up ever increasing quantities of something else

Efficiency: achieving a goal as cheaply as possible

Productive Efficiency: getting the most output from the fewest possible inputs

Inefficiency &

Unattainable

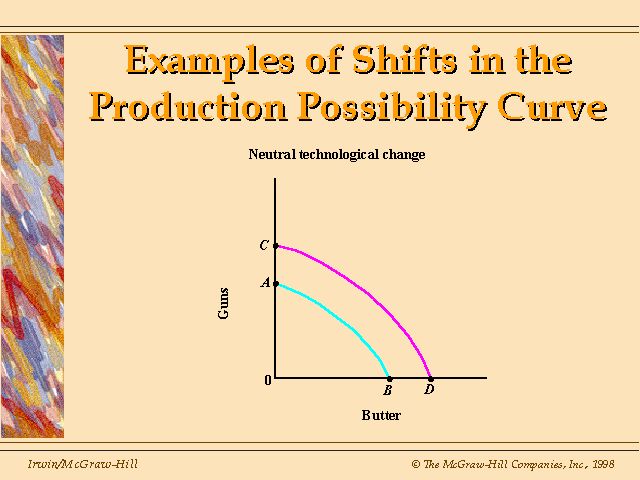

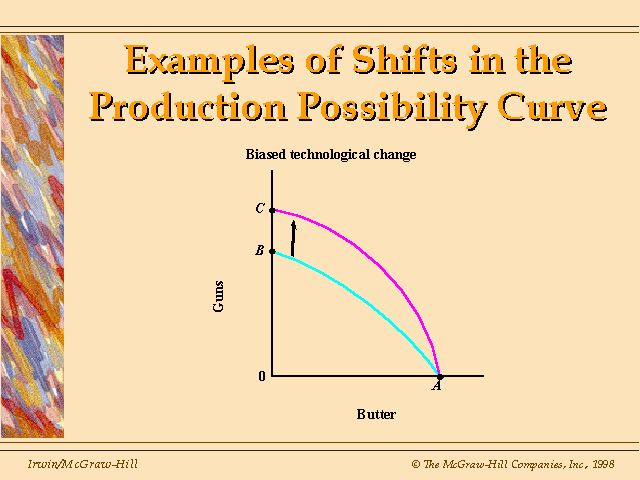

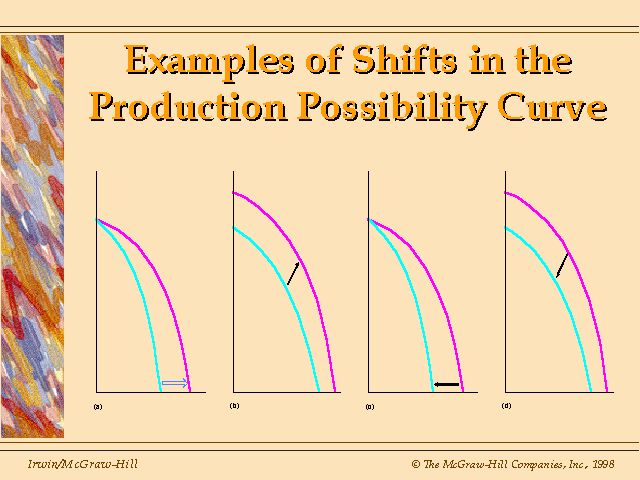

Shifts in the PPC

1. Technology improves

2. Resources discovered/destroyed (Kobe)

3. Efficiency of economic institutions

4. Population / workforce

************************************************************************************

Chapter 3

DEMAND AND SUPPLY

Some economists never leave this model

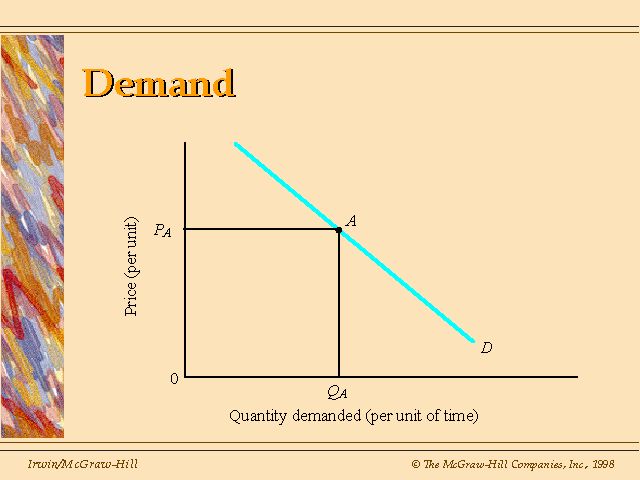

LAW OF DEMAND: More quantity of a good will be demanded the lower its price, other things held constant.

OTHER THINGS HELD CONSTANT

(Ceteris Paribus)

or...

Less quantity of a good will be demanded the higher its price, other things equal

PROBLEM: Why does the demand for cars go up every

year along with increases in P?

Law of Demand Based on SUBSTITUTION

RELATIVE vs. MONEY PRICE (nominal price)

Example=> CPI 10%, wages 10%

BUT, Jumbo Jacks

only

5%

THE DEMAND SCHEDULE (table)

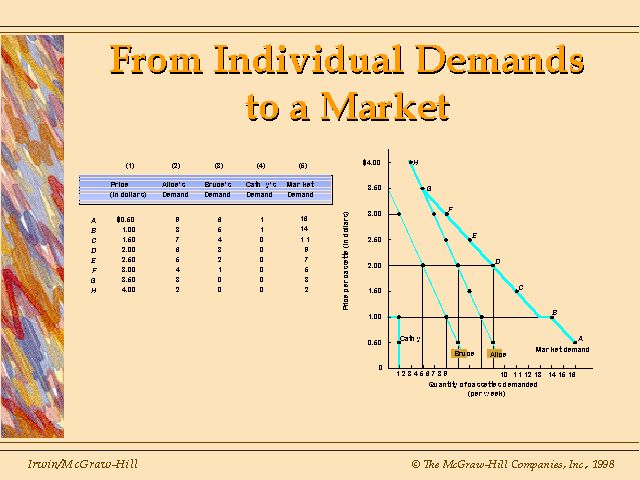

individual demand curves to market demand curve

Or, Market Demand Curves are the sum of

Individual

Demand Curves

QUANTITY DEMANDED (Qd): Q of a good that will be bought @ a specific P, other things constant

Ä Represented by a point on demand curve

A certain P & Qd combination

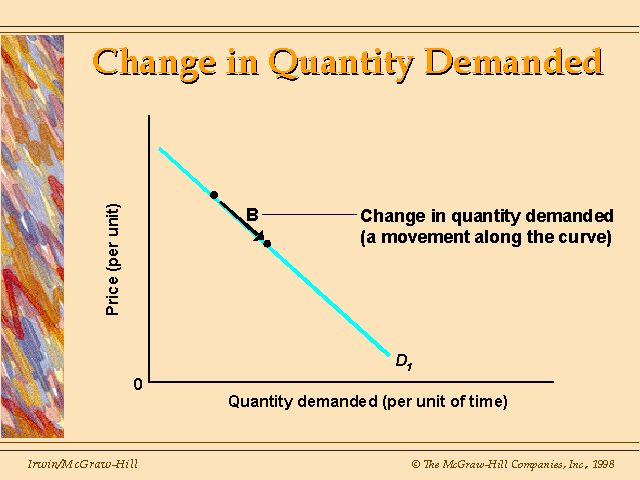

D in P causes a D in Qd = a movement along the demand curve

*Q/per unit of time

P & Q interact while other variables ceteris paribus

Partial vs. General Equilibrium

static vs. dynamic

ENDOGENOUS vs. EXOGENOUS

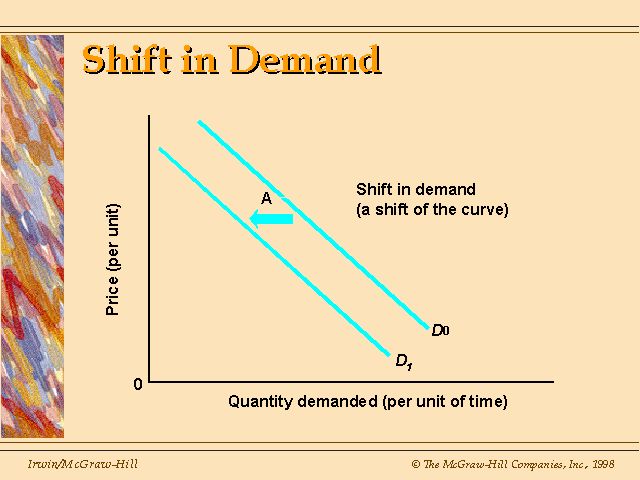

DEMAND: Quantities of a good that will be bought @ various prices, other things constant

Ä The entire

demand

curve

®If any

variable

held constant were allowed to D this would

shift

the entire demand curve

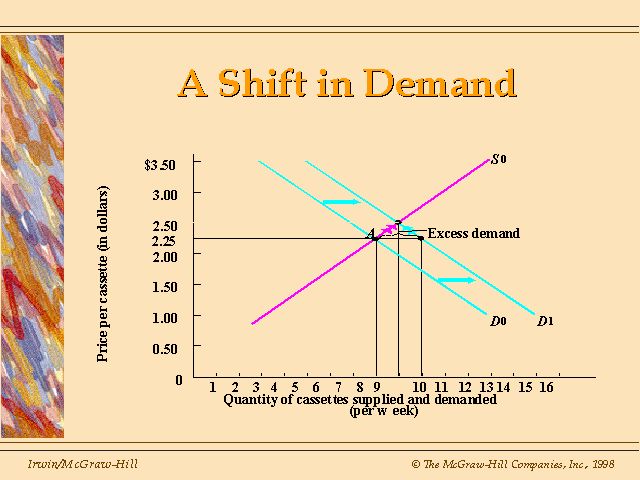

Shift Factors 1. Society’s income (population)

of Demand 2. Prices of other goods

3. Tastes & Preferences

4. Expectations

SHIFT FACTOR: something other than price that affects how much a good is demanded

**********************************************

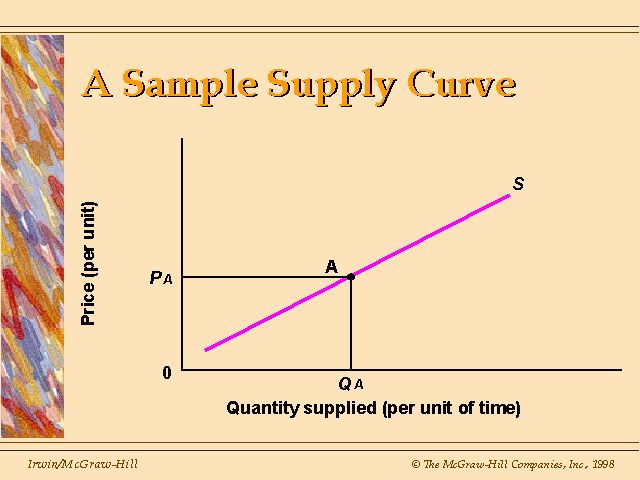

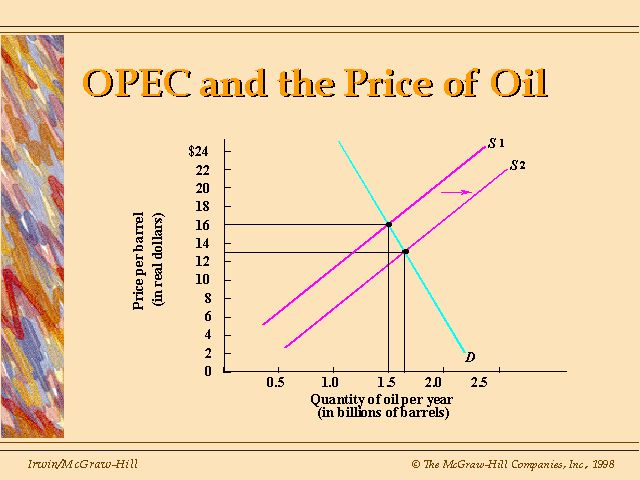

SUPPLY CURVE:

Law of Supply: Quantity supplied (Qs) of a good is directly related to the good’s price, ceteris paribus

P Qs or, P¯ Qs¯

*if price should fall firms could switch production to a higher priced good

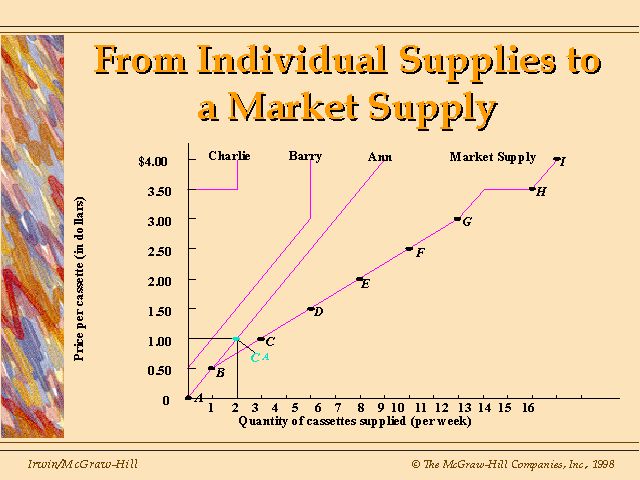

SUPPLY SCHEDULE (table)

The sum of the individual firm's supply curves

makes

the Market

Supply Curve

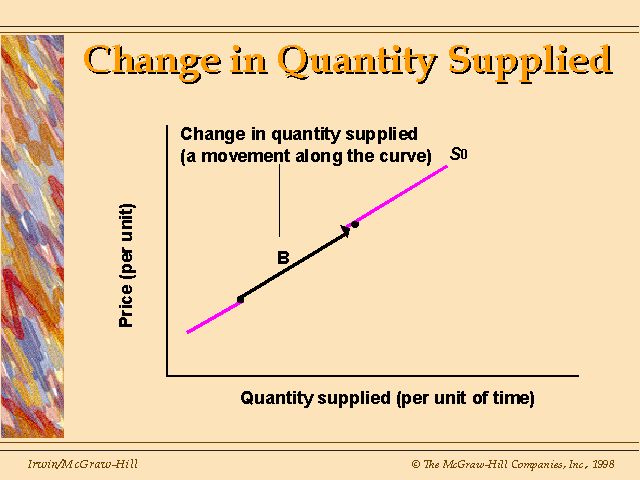

Quantity Supplied: a specific P & Qs combination, represented by a point on the supply curve

Supply: Q that will be brought to the mkt @ various prices *represented by the entire supply curve

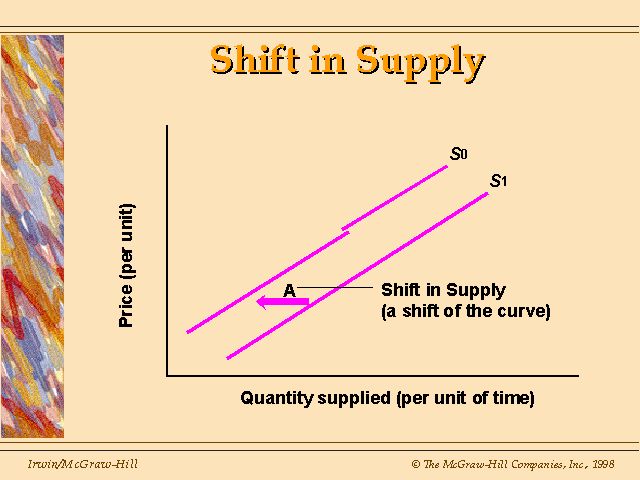

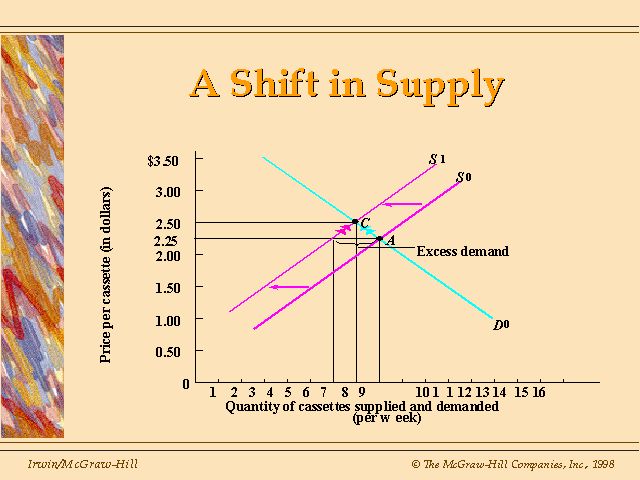

Shift Factors 1. Ds in the price of inputs

of Supply 2. Ds in technology

3. Ds in supplier’s expectations

4. Ds in taxes or subsidies

P Ds => DQs: movement along the supply curve

D shift factor

=>

D

Supply: Supply curve shifts

*******************************************************************************

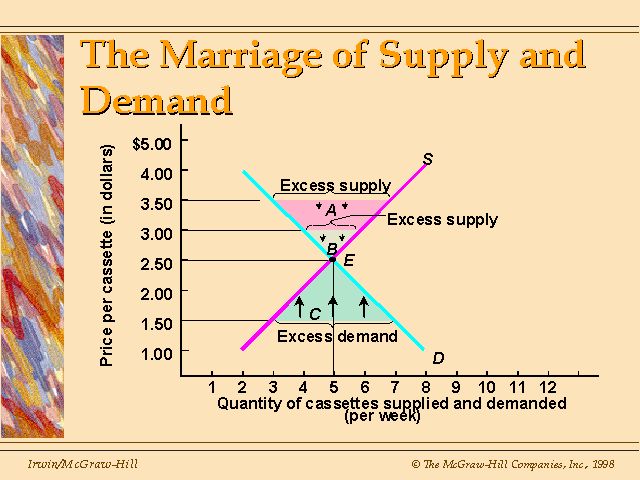

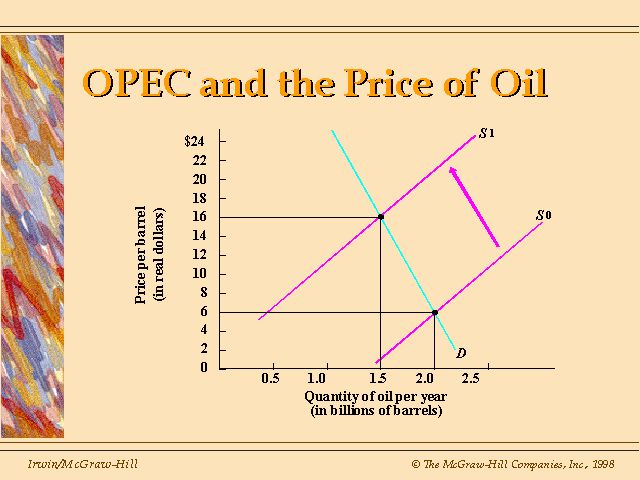

Chapter 4

1st DYNAMIC LAW OF SUPPLY & DEMAND

Qs > Qd => excess supply => P¯

Qs < Qd => excess demand => P

2nd DYNAMIC LAW OF SUPPLY & DEMAND

the greater the difference between Qd & Qs

the

greater the pressure for price to D

3rd DYNAMIC LAW OF SUPPLY & DEMAND

where S=D, Equilibrium, no tendency for P to D

Ädisequilibrium

Price Ceilings & Price Floors

***********************************************************

BUSINESS OWNERSHIP &

ORGANIZATION

Business TypesÞ

advantages

& disadvantages

NUMBERS SALES

Sole proprietorships 69% 5%

Partnerships 8% 5%

Corporations

23%

90%

Where do households get incomeÞ about 70% comes from wages

*************************************************************

Chapter 15

EXTERNALITIES, MARKET

FAILURE

& PUBLIC CHOICE

EXTERNALITY:

An

effect on a third party resulting from a transaction between two

principals,

or, a third party effecting the transaction between two principals.

FREE RIDER: A

person

who participates in something for free because others have paid for it.

PUBLIC GOODS vs. PRIVATE

GOODS

*****************************************************************

Chapter 17 (pp 378 -

379)

TYPES OF TAXES:

Progressive

Regressive

Proportional

******************************************************************

Chapter 18

INTERNATIONAL TRADE

WHY TRADE? => its benefits are all around us

Caviar, Coffee & Mangos

WORLD TRADE in 1980 dollars

1928 $245b

1935 $123b

1950 $86b

1990 $2t

***************************************************

ABSOLUTE ADVANTAGE: producing a level of output using less resources than the competition=> A. Smith

=> specialization

What if a country doesn’t have an absolute

advantage?

Does it pay for a country to trade with another

country

if it has an absolute advantage in all production compared to the other

country?

COMPARATIVE ADVANTAGE:

If production costs (opportunity costs) differ then there are gains

from

trade even if a country has an absolute advantage in producing

everything.

=> David Ricardo

U. S. Japan

Hamburgers 20 200

Samurai Swords 5 100

*assume they each use an equal amount of

inputs

to get the unequal output above

*Japan has an absolute advantage in the production of both goods => Does it pay to trade?

***************************************************

U.S. PRODUCTION POSSIBILITY TABLE

hamburgers samurai swords

20 0

16 1

12 2

8 3

4 4

0

5

Japan’s PRODUCTION POSSIBILITY TABLE

hamburgers samurai swords

200 0

160 20

120 40

80 60

40 80

0

100

WHO GAINS FROM TRADE BETWEEN A SMALL

AND A LARGE COUNTRY? small country!

***************************************************

Tariff - tax

Quota - quantity limitation

Voluntary Restraint Agreement - self imposed limit

Embargo - political trade restriction

Regulatory Restriction/U.S. beef vs. Euro wine

***************************************************

REASONS FOR TRADE RESTRICTIONS

1. Unequal internal gains trade=> trade adjustment assistance

2. Haggling by companies

3. Haggling by countries over trade restrictions

4. Specialized production

learn by doing/economies of scale

infant industry argument

5. Macro aspects

6. National Security

7. International politics - embargo

8. Increased revenue f/ tariffs

***************************************************

REASONS ECONOMISTS SUPPORT FREE TRADE

1. Free trade increases total world output - restrictions can benefit a country as long as others don’t retaliate.

2. Restrictions reduce international competition

50s & 60s => U.S. protection of domestic steel

70s uncompetitive

80s asked for tax break to retool

U.S. Steel purchases Marathon Oil

**********************************************

Free Trade Associations=> EEC & NAFTA

GATT => WTO => MFN STATUS for members only