ELASTICITY

ELASTICITY: response, or D, one variable as a result from the D another variable

Most common measure of elasticity Ä

PRICE ELASTICITY OF

DEMAND

how

much will Qd D, when there is a D

Price ??????

a measure of the % D

Qd

divided by the % D

P

% DQd DQd

Ed =

= Qd

DP

% DP

P

* Use the same formula for price

elasticity of supply (es)

TERMS:

ELASTIC: Ed > 1 industry tends to be competitive and/or the product has many substitutes

INELASTIC: Ed < 1 industry lacks competition and/or there aren’t many substitutes for the product

UNIT ELASTIC: Ed = 1

proportional

change

**********************************************************************************************

PROBLEMS CALCULATING ELASTICITY

The conventional method is to use the initial number as a reference, but an argument could be made for either number.

Ä

ARC ELASTICITY: Divide both the change in quantity & price by the sum their respective endpoints, divided by two.

(also called the midpoint formula)

D Qd

Q1 + Q2

2

_______ = Arc ed =

Elasticity

of a midpoint over a range

D P

P1 + P2

*

starting point

is the average of the endpoints

2

***********************************************************************************************

CALCULATING ELASTICITY AT A POINT

(true love vs. Jerry Seinfeld’s approach)

ELASTICITY ALONG LINEAR DEMAND & SUPPLY CURVES

Geometric

tricks for

estimating

ed & es

ELASTICITY & SLOPE (slope does not D

along a linear curve, but elasticity does)

Ed = DQ/Q / DP/P

= DQ/Q x DP/P

= DQ/DP x P/Q

=1 / DP/DQ x P/Q

= 1 / slope x P/Q

therefore, if we know the

slope

, P & Q we can determine Ed

Determinants of Price Elasticity: the influence of substitution

DEMANDÄ

1. In the long run the demand curve is more elastic e.g. ed for gas during the 70s

2. The less of a necessity, the more elastic is the demand curve, e.g., insulin vs. cheesecake

3. The more narrow a good is defined, the more

elastic

is the demand curve, e.g., cigarettes vs. Marlboro

SUPPLYÄ

1. Instantaneous, or momentary, supplyè ed <1

2. Short run supply more substitution possibleè

more elastic

3. Long run supply curve is very elastic

ELASTICITY & TOTAL REVENUE

TR = P x Q ( A = l x w )

**************************************************

OTHER ELASTICITY CONCEPTS

CROSS ELASTICITY OF DEMAND

%DQdx

=> positive sign: substitute

%DPy

negative sign: complement

% D in Qd of good X divided by the % D in the P of good Y

Cross es

Jointly produced goodsÄ

beef & leather

Cross es = % D Qsleather

% D Pbeef

positive sign/complements

INCOME ELASTICITY OF DEMAND

Ey = % DQd

=> negative sign: inferior good

% DY

positive sign: normal good

Ey>1: luxury good

Ey<1: necessity

WHO BEARS THE BURDEN OF AN EXCISE TAX????

1. Inelastic demand & supply curve shifts in

2. Elastic demand & supply curve shifts in

3. Inelastic supply

4. Elastic supply & supply curve shifts up

*inelastic pays at the extremes

General Case: $10,000 tax

graph a => tax supplier

<>graph b => tax buyerFIRMS TRY TO SEPARATE CONSUMERS WHO HAVE DIFFERENT ELASTICITIES OF DEMAND

1. AIRLINES, business vs. tourist (movies)

2. CAR DEALERS, listed price vs. people who haggle

3. SALE ITEMS, wash machines every other week on sale

********************************************************************************************

ELASTICITY & MARKET

FORECASTS

CASE ONE making adjustments to inventory

given: Ed = -2 & your price is going up by 10%

setup equation

%^Qd / 10% = -2

multiply through by 10 to isolate %^Qd

%^Qd = -20%

CASE TWO making adjustments to price to get rid of inventory

given: Ed = -4 & you want to increase sales by 20%

setup the equation

20% / %^P = -4

exchange -4 with %^P

%^P = -5%

**********************************************************************************************

Chapters 7 & 8

COSTS OF PRODUCTION

We are concerned with the short-run supply of produced goods. Chapter 10 will cover the long run.

OPPORTUNITY COST REVISITED

**********************************************************************************************

how much labor would you supply to the market?

it depends on your opportunity cost => how

much you

value your leisure time?

**********************************************************************************************

supply depends on the opportunity cost of the supplier

as the P of the factor increases the Qs of that factor expands

**This is the basis for the law of supply: When

price

increases the quantity supplied increases, ceteris

paribus

**********************************************************************************************

TERMS:

FIRM: an economic institution that transforms factors of production into consumer goods

SHORT RUN: Firm is constrained in its production decisions - some inputs are fixed

LONG RUN: The time necessary to change all factors of production - all inputs are variable>

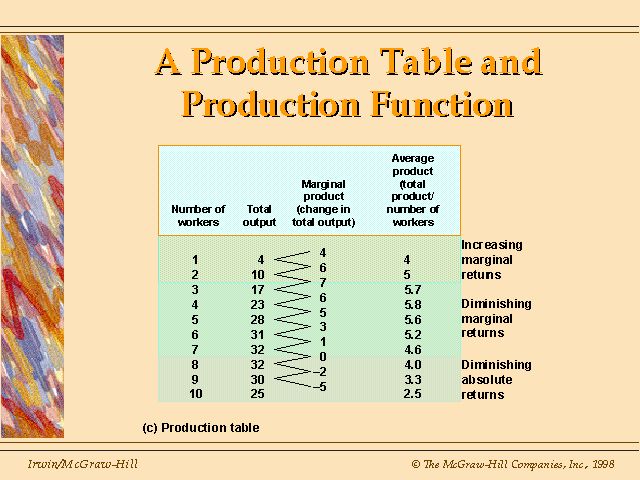

PRODUCTION TABLE: A table that

shows the output produced f/ various combinations of inputs

**********************************************************************************************

EXAMPLE

*in our example we assume inputs are fixed, except for one, labor

we will add the variable input to the fixed

inputs

& see what happens

PRODUCTION FUNCTION:

Is

a graph of the production table information

MARGINAL PRODUCT:

The

additional output produced by an additional input, ceteris paribus

AVERAGE PRODUCT: Total product divided by the variable input

***********************************************************************************************

THE LAW OF DIMINISHING

MARGINAL

PRODUCTIVITY

As more of a variable input is added to fixed inputs, the additional output one gets from the additional input will fall

***********************************************************************************************

TERMS:

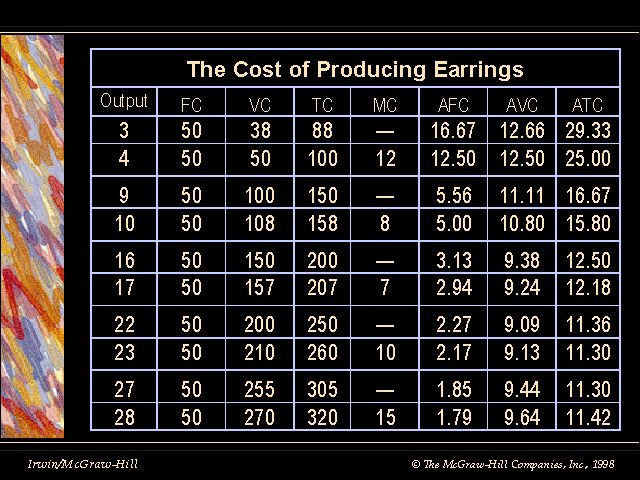

FIXED COSTS (FC): Costs that can not be changed in the time under consideration

VARIABLE COSTS (VC): Costs of the variable inputs; they change as output changes

TOTAL COST (TC): Sum of FC + VC

TC = FC + VC

*to find the average divide by Q (output)

TC = FC + VC = ATC = AFC + AVC

Q

Q

Q

ATC = TC/Q

AFC = FC/Q

AVC = VC/Q

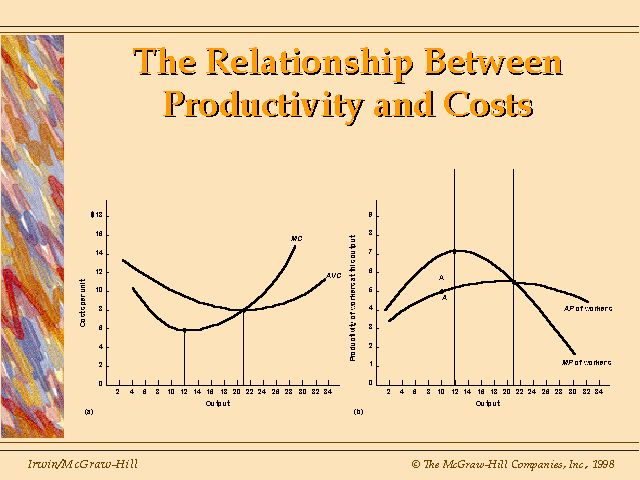

Marginal Costs: cost of increasing output by one unit (MC)

u-shaped MC curve; AVC curve & ATC curve

Initially marginal product increases & costs fall (MC, AVC & ATC). Then "The Law of Diminishing Marginal Productivity" sets in & MP falls forcing costs up (first MC, then AVC and finally ATC).

MC < AVC, then AVC is falling

MC = AVC, then AVC is @ a minimum

MC > AVC, then AVC is rising

MC < ATC, then ATC is falling

MC = ATC, then ATC is @ a minimum

MC > ATC, then ATC is rising

Chapter 9

Supply decisions in the long

run => all inputs are variable

=============================================

Production decisions are based on

Available Technology & Cost

Technical Efficiency: using the least amount of inputs in the

production of a given output

Economic Efficiency:

the lowest cost method of production for a given level

of output

=============================================

production of identical products in different

countries

depends

on the price of inputs

U.S. vs. Mexico => clothes

U.S. vs. China => roads

=============================================

Technical Efficiency is not always Economic Efficiency

this depends on the

level

of output

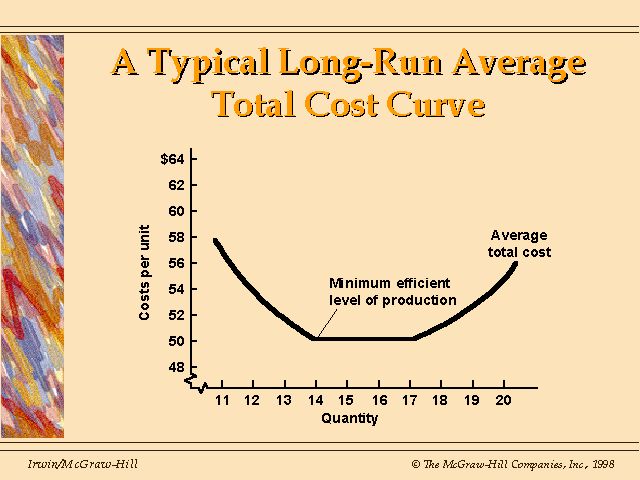

Indivisible set-up costs:

an investment in technology that would only payoff after a MINIMUM

EFFICIENT LEVEL OF PRODUCTION

=============================================

E.G., Pontiac Fiero (200,000) vs. Mazda Miata (30,000)

=============================================

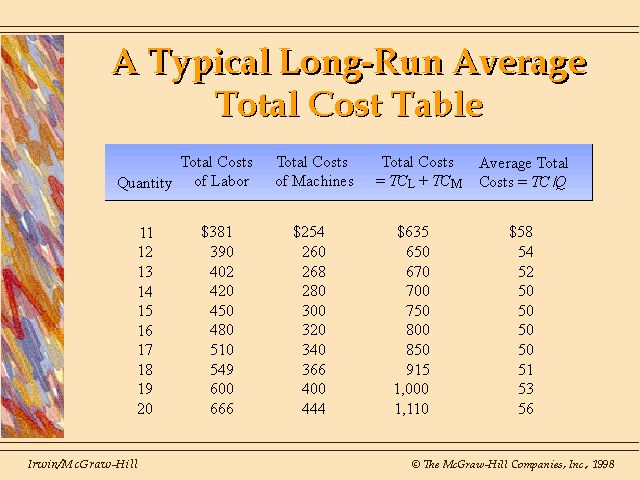

WHAT SHAPES THE LR COST CURVE?

Short-run cost curve is u-shaped because of the law of diminishing marginal productivity

*but in the long run all inputs are variable

Long-run cost curve is u-shaped because of :

1. Economies of scale: cost per unit fall as output rises, e.g., Henry Ford

2. Diseconomies of

scale:

an increase in per unit cost as output rises,

e.g., firm too big

a. Monitoring Cost

b. Team Spirit

Importance of Economies & Diseconomies of Scale

Economies of scale promotes expansion/mergers

Diseconomies promote contraction/takeover defense

Raiders

Real-World Issues:

1. Economies of scope: costs of production are interdependent - costs savings for one product because of producing another. E.G., Purina/Jack-in-the-Box, Pepsico

2. Learn by Doing: firms become more efficient over time w/out any changes in inputs

3. Technological change shifts the cost curve down

4. Unmeasured costs/ accounting vs. economics