True/False Answers

Definition of Economics

1. Scarcity is a problem only for the poor.

Ans. F Scarcity exists because people's wants exceed their ability to meet those wants, and this fact of life is true for any person, rich or poor.

2. Macroeconomics studies the factors that change national employment and income.

Ans. T Macroeconomics studies the entire economy; microeconomics studies separate parts of the economy.

Three Big Microeconomic Questions

3. Answering the question “What goods and services are produced?” automatically answers the question, “How are goods and services produced?”

Ans. F Almost always, goods and services can be produced many different ways, so the “how” question must be answered separately from the “what” question.

4. An example of the “how” question is: “How does the nation decide who gets the goods and services that are produced?”

Ans. F The “how” question asks, “How are goods and services produced?”

Three Big Macroeconomic Questions

5. “For whom are goods and services produced?” is one of the big macroeconomic questions.

Ans. F The “for whom” question is one of the three microeconomic questions.

6. A rising cost of living is called inflation.

Ans. T A rising cost of living is the definition of inflation.

7. In a business cycle, an expansion follows the peak.

Ans. F A recession follows the peak. An expansion follows the trough.

The Economic Way of Thinking

8. Tradeoffs mean that you give up one thing to get something else.

Ans. T The question gives the definition of a tradeoff.

9. There is no such thing as a “how” tradeoff because a business uses only way to produce its products.

Ans. F Businesses almost always can produce their products many different ways, so they face a “how” tradeoff when they choose which method they will use.

10. The output-inflation tradeoff refers to the point that lowering inflation increases output.

Ans. F The output-inflation tradeoff refers to the point that lowering inflation decreases output.

11. The opportunity cost of buying a slice of pizza for $3 rather than a burrito for $3 is the burrito.

Ans. T The opportunity cost is the burrito that was foregone in order to buy the pizza.

12. By comparing the cost and benefit of a small change you are making your choice at the margin.

Ans. T The definition of making a choice at the margin means that choice revolves around a small change.

Production Possibilities and Opportunity Cost

13. In Figure 2.4 point a is NOT attainable.

Ans. F Any point on the production possibilities frontier is attainable, even points where the PPF intersects the axes.

14. In Figure 2.4 the opportunity cost of moving from point b to point c is 10 computers.

Ans. T The opportunity cost equals the number of computers foregone, in this case the fall from 30 computers at point b to 20 at point c .

15. From a point on the PPF , rearranging production and producing more of all goods is possible.

Ans. F Points on the frontier are production efficient, so increasing the production of one good necessarily requires producing fewer of some other good.

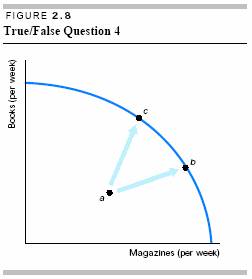

16. From a point within the PPF , rearranging production and producing more of all goods is possible.

Ans. T Points within the frontier are inefficient, which means its possible to rearrange production and boost the production of all goods and services. This condition is illustrated in Figure 2.8, where from (the inefficient) point a , it is possible to move to points such as b or c where more of both books and magazines are produced.

17. Production efficiency requires producing at a point on the PPF .

Ans. T Production efficiency implies that the production of one good can be increased only if the production of another good is decreased, which is true only on the PPF itself.

18. Along a bowed-out PPF , as more of a good is produced, the opportunity cost of producing the good diminishes.

Ans. F As more of a good is produced, the opportunity cost of additional units increases.

Using Resources Efficiently

19. The marginal cost of the 20th ton of cement equals the cost of producing all 20 tons of cement.

Ans. F The marginal cost is the cost of the 20th ton itself, not the cost of producing all 20 tons.

20. As people have more of a product, the product's marginal benefit decreases.

Ans. T As people have more of a product, they are willing to pay less for additional units, which means that the marginal benefit of the product will decrease.

21. Efficiency is achieved by producing the amount of a good such that the marginal benefit of the last unit produced exceeds its marginal cost by as much as possible.

Ans. F For resources to be allocated efficiently, it is necessary for the marginal benefit of the last unit produced to equal the marginal cost of the unit.

Economic Growth

22. Economic growth is illustrated by outward shifts in the PPF .

Ans. T As the PPF shifts outward, the nation is able to produce more of all goods.

23. Increasing a nation's economic growth rate has an opportunity cost.

Ans. T The opportunity cost is the loss of current consumption.